How is Your Credit Score Calculated?

Have you ever wondered “how your credit score calculated?” Have you asked, but are always given vague answers? Ever questioned what credit models are used? Wonder no more. We will tell you exactly how credit scores are determined for most people and then allow you to get a rough estimate of what your credit score might look like.

5 Key Factors to Calculating Your Credit Score

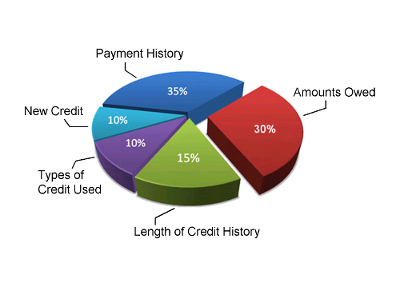

1. Payment History (35%)

Your payment history is the most important factor in your credit score. Creditors want to know if you are going to pay them back. So payment history will usually make up 35% of your credit score. Your credit bureau payment history takes into account all payments on all of your consumer debts: your credit cards, line of credit, car loan, etc. Your credit report payment history will look at how many accounts you have that are paid as agreed, how many past due payments you have, whether or not you have any adverse public records (bankruptcy, judgments, liens, etc.) or collection activities. It will also calculate the recency of any late payments or collection activities.

2. Amounts Owed (30%)

When you apply for credit, the amount of consumer debt you owe, your available credit, and your credit utilization ratio really matters to a lender. If you are close to maxing out all of your credit cards or your line of credit, this could be a sign that you are in financial distress, and it means that you are a higher risk to lenders—statistically speaking. This is why the amounts that you owe on your debts make up 30% of your credit score. This part of your credit score will look at the amounts you owe on each credit card, line of credit and loan (including auto loans, mortgage loans, and any installment loans) you have. It will look at the number of accounts you have with balances and what percent you are using of each of your credit limits. If you are using 75% or more of your credit limit on a credit card or line of credit, this is seen as a sign of trouble and your credit score will be negatively impacted.

3. Length of Credit History (15%)

If you have had credit available to you for a long time, your credit report should provide an accurate picture of how you use it. For someone who has not had credit for very long, it is difficult to tell if they really know how to use credit responsibly. Time is needed to get a true picture of how responsible someone is with credit. This is why the length of your credit history is the third most important factor in your credit score calculation. It will usually make up 15% of your credit score. Your score will reflect how long it has been since you first obtained credit, how long each item on your credit report has been reporting and whether or not you have active credit right now. If you have recently obtained credit for the first time, your credit score will not be very strong. However, if you have been responsibly using credit for many years, this factor will really work for you. If you have been involved in a bankruptcy, consumer proposal or debt management program, your credit history will essentially restart whenever you complete your program (the record of your program also has to fall off your credit report for you to get a good credit score).

4. New Credit (10%)

If you are frequently applying for credit, your creditors want to know. This can mean that you’re in a desperate financial situation, and this could mean that you are now a riskier customer to your creditors and credit card issuers. This is one reason why new credit and credit inquiries compose around 10% of your credit score. This part of your credit score will take into account the number of credit accounts you have opened recently, the number of recent credit inquiries, the time since any new accounts were opened and the time since your most recent credit inquiries. This part of your credit score will also evaluate whether or not you are re-establishing good credit history follow past payment problems.

5. Types of Credit Used (10%)

Creditors are interested to see if you have experience handling different kinds of credit. Even though this part of your credit score makes up 10% of the total, it is the least significant unless you don’t have much other information on your credit report. Even though the credit scoring system looks at a credit mix, you shouldn’t go around applying for different types of credit or credit card accounts to try to improve your score in this area. Only open credit accounts as you need them. This part of the credit score is likely in place to help identify people who abuse credit or people who apply for every credit card that comes in the mail. If you focus on being responsible with your credit, this part of your score will most likely take care of itself.

Other Factors

The weighting of each key factor that we have outlined applies to the majority of consumers—but it doesn’t apply to everyone. If you don’t have much information on your credit report or if you have new credit, then the credit scoring system will weigh these factors a little differently. The system may also alter the weighting of each factor for people with different kinds of credit histories. The weightings presented here are the best estimates that can be given for the majority of the population.

The factors discussed here are also not the only things that are important when you apply for credit. Lenders will consider other factors as well. They will look at your income, your assets, how long you have been at your job and the reasons why you are applying for credit.

If you want to know what your credit score is, you can request it from credit bureaus like Equifax or Trans Union, but they will charge you money to get it. If you don’t want to pay anything, you can use this credit score estimator to get a rough idea of what your credit score might be. You can also play around with this calculator and try out different scenarios if you like.

For more detailed information about credit scores and credit reports, you can take a look at a government publication called “Understanding Your Credit Report and Credit Score.”

0 Comments