Avoid Bankruptcy with Alternatives – Consumer Proposal, Debt Consolidation, Debt Settlement, Debt Management Program

There are a lot of alternatives and ways to avoid bankruptcy that most people don’t know about. Money and debt problems aren’t talked about. Neither is what you can do and what your options are when you aren’t able to pay your bills and debts.

Not knowing which questions to ask or where to turn for help makes it that much harder when you try to find what you can do instead of declaring bankruptcy. Other times, the fees associated with filing for bankruptcy can be the reason why someone wants to avoid going through the process.

Directly below are 4 common alternatives to bankruptcy that one of our Credit Counsellors will be happy to explain to you. If you’d like a little more insight, further below is a chart that compares different debt relief options so you can see more of the differences between various options.

Consumer Proposal vs Bankruptcy – Know the Difference

A Consumer Proposal is a way to consolidate your debts and only repay part of what you owe. It is a legal arrangement under the Bankruptcy and Insolvency Act with its own set of rules, conditions and fees. A bankruptcy trustee arranges your proposal and the creditors who hold the majority of your debt must agree to the conditions.

Here is more information about Consumer Proposals vs Bankruptcy, including the major differences between the two, the costs of each option, how they effect your assets, how long each process takes, how they impact your credit, and the long-term consequences. Find out about this alternative to bankruptcy and see if it may be right for you.

Debt Consolidation – Choose the Best Way to Consolidate Your Debts

Consolidation Loan, Home Equity Loan, Line of Credit, Debt Management Program, Debt Settlement, Consumer Proposal, Borrow Money

There are two main types of debt consolidation. Type one requires borrowing more money to consolidate your loans, credit cards and other unsecured debts into one new loan. You need to be able to qualify for a new loan, or the increase of an existing loan or mortgage, for this option to work. Borrowing more money can end up increasing what you owe, even with a mortgage home equity loan, rather than helping you pay off your existing debts.

Debt Repayment Program or Debt Management Program (DMP)

The second main kind of debt consolidation involves consolidating just your payments into a repayment program you can afford. This type of program, when done through a non-profit credit counselling agency like ours, is also called a Debt Management Program. It does not involve borrowing more money, which helps someone avoid the risk of getting deeper into debt.

You can learn more about this option or talk to a Credit Counsellor to find out if it might be a good option for your situation.

Debt Settlement – Is it Your Best Option? Explore Our Services and Helpful Tips

Settling your debts for less than what you owe is only an alternative, or a way to avoid bankruptcy. It’s also a way of getting relief from your debts if you have a lump sum of money available to offer your creditors.

As with other debt relief options, creditors need to agree to your offer ahead of time. They also need to agree to write off any remaining balance.

Here is more information about debt settlements, how they work and what to watch out for. Just like with any tool, if a debt settlement is used the right way, it may be the right option to help you. If it’s used the wrong way, it can snowball into a financial and legal disaster.

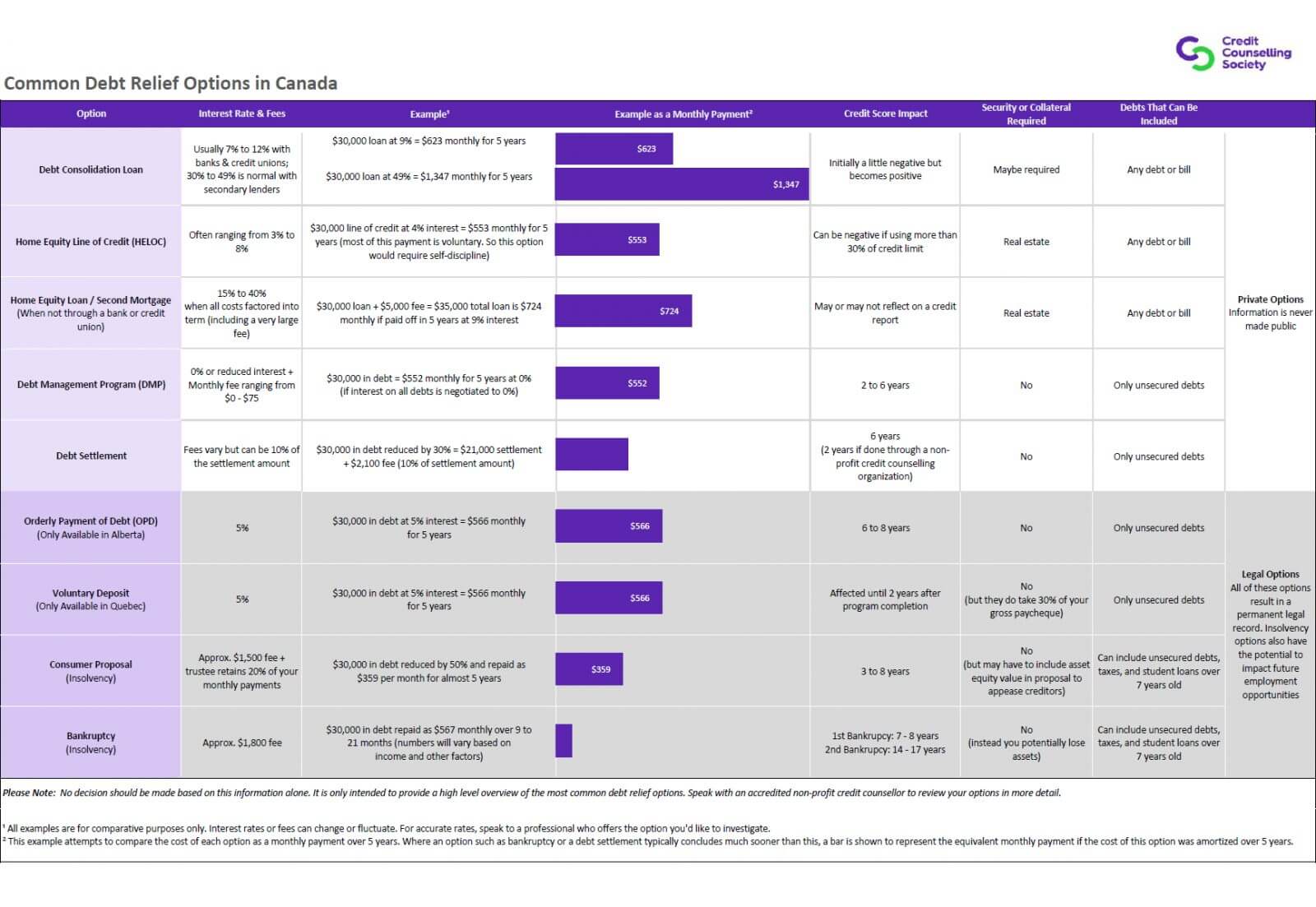

Comparing Popular Debt Relief Options in Canada

If for more information on the bankruptcy alternatives mentioned here plus some more details on each one, check out the comparison chart below. It shows you more of the pros and cons of each option. However, it’s only a high level summary. For more complete information or to see how any of these options would apply to your situation, either contact a professional who offers that option or speak with a professionally accredited, non-profit Credit Counsellor.

Common Questions About Bankruptcy

If you are struggling to pay your debts and need more information about how to avoid bankruptcy and explore alternatives, contact us to get help determining your options. One of our Credit Counsellors will answer your questions and provide you with guidance and information so that you can make an informed decision. Contact us today by phone at 1-888-527-8999, by email or chat with us online right now.

Putting Your Interests First

Our goal is to always put consumers first and look out for their best interests in everything we do. One way we do this is through transparency and accountability. We are held accountable to the most rigorous standards in our industry.